I toured a $9 million house in Honolulu to better understand the luxury housing market. I love real estate, and visiting nice homes for sale is one of my favorite hobbies.

My parents are 81 and 78 and live in Honolulu. Like many people their age, they have a few health issues, and I'd like to be there to help take care of them.

Since we're flexible and can live anywhere, my wife and I plan to relocate to Honolulu in 2029, once the school entry timing works for our kids. There, we'll take my parents to doctor appointments, fix things around their house, get them food, and simply spend more time together while we can.

A home purchase that far out is one of the biggest financial decisions we'll ever make, so I'm studying the market years in advance. Touring open houses is free education. The more homes you see, the better calibrated you become on value, and the less likely you are to make an emotional mistake when it's finally time to buy.

That's how I found myself standing in a 6,700 square foot estate in Kahala with my wife, my dad, and our two kids. Five bedrooms, 5.5 baths, a free-form pool with a hot tub and cold plunge, a koi pond, and a gym with a climbing wall all on about at 15,000 sqft lot. It was sweet!

The house had been sitting on the market for over 200 days, which made it a perfect case study. Who buys these homes? And why was nobody buying this one?

The Family Verdict Took About Ten Minutes

My wife's review: it feels too big. She's right. We're a family of four. We'd realistically use a kitchen, a family room, four bedrooms, and the pool. The other 3,000 square feet would exist mainly to be cleaned, cooled, insured, and repaired.

My dad's review was more sobering. The stairs were difficult for him. In one sentence, he eliminated an entire category of homes from our future search. Any home we buy should probably be on a single-level, or at least have a single-level ohana unit.

Then there's the empty nest math. Our youngest heads to college in 12 years. Soon after we'd move in, it would be two adults rattling around 6,700 square feet like two marbles in a shoebox. That's 3,350 square feet per person, plus an estimated $3,000 to $4,000 a month for the pool, tropical landscaping, and koi pond maintenance, before property taxes and insurance. Call it $150,000+ a year to maintain rooms we'd visit like museum exhibits.

So the house is a no for us at this price. But the tour raised a better question. If a family that could stretch for this home finds it impractical, who is actually buying at this price point?

I spent an hour talking with the listing agent to find out. Her answer was insightful.

“Most Buyers At This Price Point Are Buying Second Homes”

According to her, many buyers of $8-$10 million Honolulu homes don't live in them full-time. Recent interest has come from Japanese nationals and West Coast buyers purchasing second homes they might use a month or two a year. Given the price points, I have to imagine many are entrepreneurs who had liquidity events, because even a $1 million a year W-2 job doesn't comfortably support a $9 million vacation home.

Let that sink in. Someone pays $9 million for a house, plus $150,000 a year in carrying costs, to use it 30 days annually. Amortize the carrying costs alone and you're at roughly $5,000 per night of actual use. Then there's the $380,000 a year in risk-free income you could earn off $9 million. So we're really talking more like $20,000 a night to live in the house for 30 days, or $10,000 a night if you visit for two months a year.

I guess that's not terrible, especially if the housing market continues to go up. But that's still quite a bit of money when you can stay at a resort for far less.

As someone who spent 13 years working in equities and 17 years writing about money, I couldn't compute it. So I kept digging until I found the answer to these mega luxury purchases.

Here's what I found. The rich don't justify these purchases. They've simply graduated past the need to.

Justification #1: The Denominator Is Different

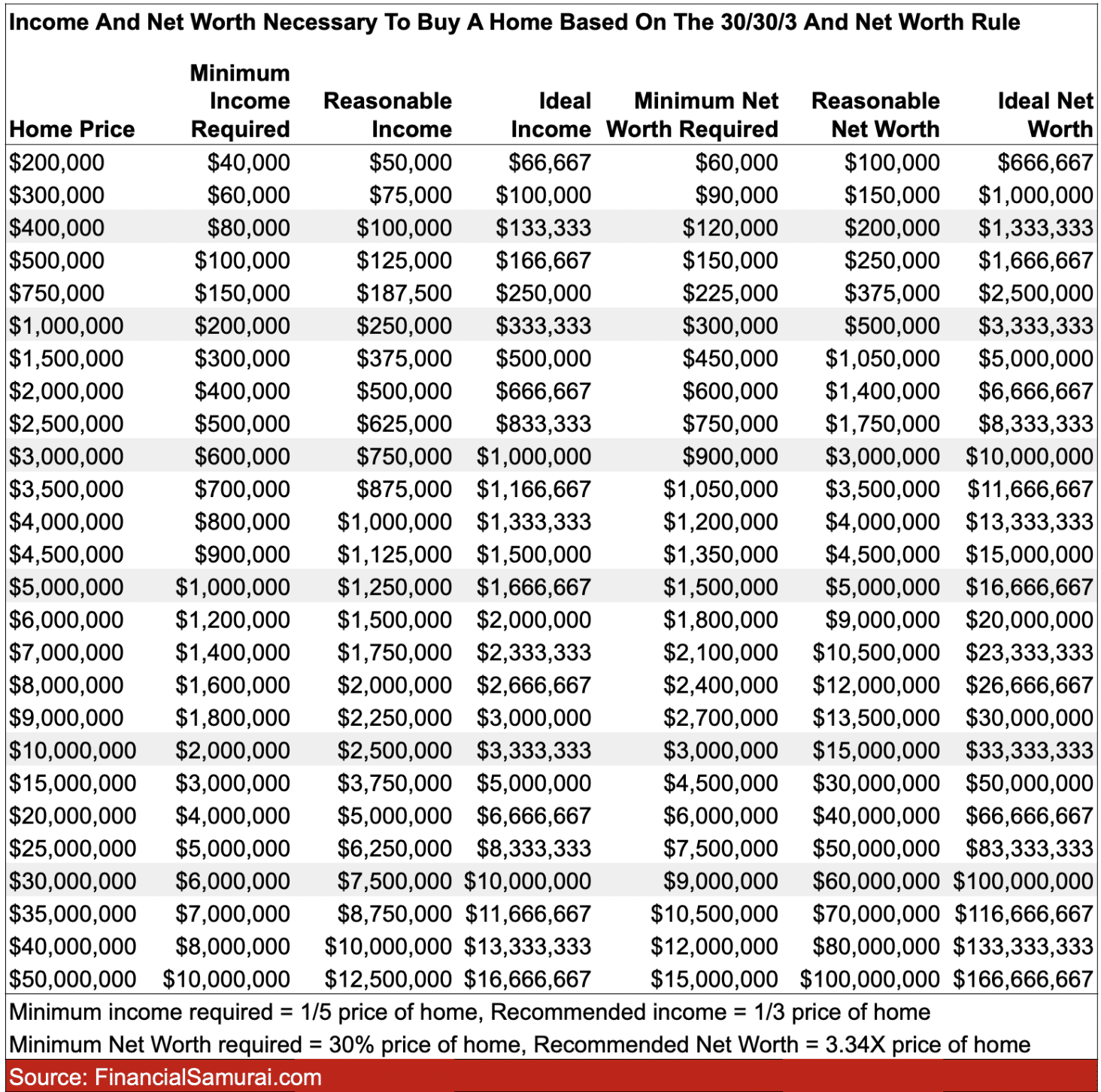

My net worth rule for home buying says keep your primary residence at 30% of net worth or below, ideally closer to 20%. Violate it and the house starts owning you. So that would mean at least a $30 million net worth, and ideally, $45 million.

If you're thinking of upgrading to a bigger, more expensive home, check out my income and net worth requirements to buy a home at all price points. It combines my 30/30/3 home buying rule with my net worth rule to show the minimum and ideal figures for homes priced from $200,000 all the way up to $50 million. Follow the guide and you'll buy with confidence instead of buying with heartburn.

But the typical buyer of this home isn't stretching. They're likely worth $100 million to $300 million. At $150 million, an $9 million house is just 6% of net worth. That's the equivalent of a household with a $1.5 million net worth buying an $90,000 condo. Nobody writes think pieces about whether that's irresponsible because it’s not.

The rule I recommend isn't wrong. Their denominator is just so large for the rich the rule never gets tested. When your second home could burn down uninsured and your lifestyle wouldn't change, the question “can I afford this?” stops being a question.

The wealthier people get, the smaller the percentage of net worth they tend to spend on their primary residence. The ultra-rich have the lion's share of their wealth in businesses and investments. The $9 million Kahala buyer isn't breaking my rule. They're following it to an extreme.

Justification #2: The House Is A Vault With A Pool

The ultra-wealthy don't think of a vacation property estate as only shelter. They think of it as a store of wealth.

Hawaii is not making more land next to the ocean. Supply is permanently constrained, global demand keeps rising, and trophy properties in world-class locations have historically held value like fine art, except you can swim in this art.

For international buyers, it's also a currency and stability play. A hard asset in a politically stable jurisdiction, denominated in dollars, that your family can enjoy or escape to if things go sideways back home.

With the yen having weakened significantly against the dollar over the years, Japanese buyers who hold dollar assets or dollar-earning businesses are also playing a longer currency game than most of us bother to think about.

The month of annual use is incidental. The house is functionally a bond that happens to have a lanai. I've long argued real estate acts as a bond plus equivalent in a portfolio. The ultra-rich just take the concept to its logical extreme.

Justification #3: The Estate Planning Angle

When you die, assets included in your taxable estate receive a stepped-up cost basis to fair market value. Buy the Hawaii house for $9 million, hold it until it's worth $20 million at death, and your kids inherit it with a $20 million basis. If they sell immediately, they owe essentially zero capital gains tax on $11 million of appreciation.

Now, before you conclude the rich pay no taxes, the estate tax still applies. In 2026, the federal exemption is $15 million per person, or $30 million per couple, with a 40% rate above that. A $150 million estate is still writing the IRS a check for roughly $48 million if the assets are not in a GRAT or dynasty trust. Hawaii also levies its own estate tax of up to 20% on Hawaii real property, even for out-of-state owners, a detail I suspect half these buyers never priced in.

So the step-up isn't a tax dodge. It's basis arbitrage. Wealthy families deliberately keep low-basis assets like real estate inside the estate to capture the step-up, while gifting high-growth assets out early to dynasty trusts. The estate tax was going to hit their retained assets at 40% anyway. The step-up wipes out decades of capital gains as a consolation prize.

The house isn't just a vault. It's a pre-positioned inheritance, professionally gift-wrapped by an estate attorney everybody should talk to. Ironically, the poorer you are, the more important it may be to get your estate in order given probate court is far more expensive than distributing assets through a revocable living trust.

Justification #4: They're Paying For Optionality, Not Occupancy

I've written for years that money's greatest return is freedom. This is why the FIRE movement is so attractive. I'm happy to give up making more money to have more freedom. The ultra-rich apply this to real estate.

They aren't buying 30 days of use. They're buying the perpetual option to wake up tomorrow and decide to spend a month in Hawaii, with their own sheets, their own coffee maker, and nobody else's hair in the shower drain. The empty 335 days don't bother them because occupancy was never the point. The ability to occupy was.

Is that an insane price for optionality? By my math, yes. But we also pay for optionality constantly, just with more zeros removed. We have a paid off vacation property in Lake Tahoe worth about $750,000. It’s been a terrible investment. But it’s now a great lifestyle investment after our kids were born. The principle is identical. Only the scale offends.

Justification #5: They Don't Do Cost-Per-Use Math Like The Rest Of Us

This was my final realization, and the most humbling one.

I calculated cost per night. I calculated price per occupied square foot post-empty-nest. Then I calculated carrying costs as a percentage of a safe withdrawal rate.

The ultra-rich do things differently. They vibe coded the numbers based on their feelings.

Cost-per-use math is a middle-class and mass-affluent survival skill. It's how people like us built wealth in the first place. But past a certain net worth, the skill atrophies because it no longer serves a purpose.

When someone worth $200 million buys a $9 million house, asking them to justify it is like asking you to justify buying a $12 sandwich. Justify it to whom? It doesn't matter.

That's the real answer to my perplexity. I was asking a question the buyers stopped asking themselves a decade and eight figures ago.

The Takeaway

If you've ever felt behind because someone bought a house that seems impossibly expensive, understand you're likely watching a different game with different rules. The buyer isn't braver or smarter than you. They just have a denominator so large the decision required no courage at all.

Meanwhile, keep doing what actually works. Tour homes years before you plan to buy. Bring the people who will live in and visit the home, because your family will spot dealbreakers a listing photo never will.

Keep running your cost-per-use math. Keep your primary residence at 30% of net worth or less. And before you upgrade to a bigger, more expensive home you don’t need, run your numbers against my home buying guide below.

Being house rich and cash poor is no fun. You will likely be stressed out of your mind for the first year if you violate my guide above.

The discipline that seems unnecessary to the ultra-rich is exactly the discipline that might get you to their side of the table. And if you get there, I suspect you'll keep doing the math anyway. Old habits built your wealth. No koi pond should retire them.

Readers, how do you explain paying $9 million for a home you use one month a year? Have you ever toured homes way above your price range to learn the market? And at what net worth, if any, would you stop doing cost-per-use math?

Invest In Real Estate Passively

To invest in real estate without the carrying costs, koi ponds, or climbing walls, check out Fundrise. Fundrise manages over $3 billion for investors, primarily in residential and industrial properties in the Sunbelt, where valuations are lower and yields are higher.

The ultra-rich buy $9 million Hawaii homes as stores of wealth because they can afford to lock up capital in a single illiquid asset. The rest of us can capture the same benefits, income, inflation protection, and diversification away from stocks, for as little as $10 and zero koi pond maintenance. I've personally invested over $500,000 with Fundrise to earn passive income and diversify my expensive San Francisco real estate holdings. Fundrise is a long-time sponsor of Financial Tips.

For more nuanced personal finance content, join 60,000+ others and sign up for the free Financial Tips newsletter. Financial Tips began in 2009 and is one of the most trusted independently-run personal finance sites today. Everything is written based on firsthand experience because money is too important to be left up to pontification.

Sam,

I’ve been following you for years, and this was another fascinating breakdown. The math on how the ultra-wealthy view real estate as a “vault with a pool” to hedge against inflation makes perfect sense. I say this as someone who has built an 8-figure net worth primarily through real estate investments while working a high-paying job in tech. I understand the instinct to optimize the numbers, protect the downside, and look for the smartest play.

But what struck me most about this post wasn’t the $9 million arbitrage—it was your opening note about your parents being 78 and 81 in Honolulu, and your desire to be closer to them.

If there is any lesson I have learned about how the wealthy spend their money, it’s that they are ultimately buying control over their time and options.

I lost my parents unexpectedly, and much too soon. I learned from that heartbreak that the math on time with aging parents doesn’t operate on standard financial rules. Like the luxury buyers you described, you can’t use “cost-per-use” logic when calculating the value of a Tuesday afternoon coffee or an impromptu dinner with your mom and dad.

At 78 and 81, the runway isn’t theoretical anymore. Health can pivot in a single afternoon. From one real estate investor to another: you have won the game. You’ve mastered the mechanics of wealth, optimized the denominators, and built an incredible safety net. Now is the time to deploy that capital to buy the ultimate luxury: proximity to the people who matter most, while they are still here to enjoy it with you!

Don’t wait for the perfect real estate market, the perfect cycle, or the “right” time to transition. Tour the homes, find a place, and make the move sooner rather than later. Speaking from experience, you will never look back on your life and wish you spent more time optimizing a portfolio, but you will always cherish every extra day you got to spend in the same zip code as your parents.

Pull the trigger. Go home to Hawaii.

Great advice. And I agree. Life is way too short, and I’m here with my parents for the entire month of July, and will come back again in the fall or winter for a couple of weeks. It’s not enough, but I’m doing my best to be there for them as I figure out schools and housing, as well as balancing my wife’s desires as her parents are on the East Coast.

Just toured another home today. Pretty nice!

Sam, such an interesting article. Really thought provoking and not sure lf there is a correct answer. Do you have a rule of thumb for second houses like this article? Eg not more than 50% of primary and/or 10% of total..and/or not more than 3x what you would pay for a airbnb rental on a nightly basis equivalent or something??

Been scratching my head about a holiday home for years and can’t make it work mentally. The cost is known but that is essentially the price for the memories being created.

Here are some relevant rules for a second home / vacation home:

https://financialtips.biz/the-only-time-you-should-consider-buying-a-vacation-property/

https://financialtips.biz/a-vacation-property-buying-rule-to-consider/

In general, I don’t recommend it! And this comes from someone who has owned a vacation home since 2007 in Lake Tahoe. But it’s great for lifestyle. Just bad for money.

Fascinating analysis on the ultra-wealthy’s real estate strategies.

What’s often overlooked is that these “underutilized” properties

aren’t just status symbols—they’re strategic wealth preservation

tools. The rich understand that prime real estate in appreciating

markets serves as both an inflation hedge and a tax-advantaged

store of value.

At deWealthy.com, we’ve been analyzing similar patterns among

high-net-worth individuals in tier-1 markets. The key insight:

it’s not about “using” the property—it’s about capital allocation,

wealth transfer strategies, and portfolio diversification that

most conventional analyses miss.

The real question isn’t whether they “need” 9-million-dollar homes.

It’s whether these assets outperform traditional investments over

10-20 year horizons. Based on historical data in markets like SF,

NYC, and London, the answer is often yes—especially when you

factor in leverage, depreciation benefits, and appreciation.

Would love to hear your thoughts on how middle-class investors

can apply similar principles at smaller scales. Great piece, Sam!

Yeah, I don’t think people realize how much wealth there really is out there. The middle class/mass affluent dual income household trying to keep up by sending kids to private schools and buying mansions are going to lose the battle.

Stealth wealth is reigning supreme. Don’t be fooled regular hustling people! You will never catch up unless you take more risks or get to the top 1% in your organization.

This is why we read FS. A great thought piece and something most of us have never considered. It’s about the zeros! Thanks for continuing to educate us.

My oh my that does sound like a lot of house. At some point the larger a home is the more it’s “required” to have a team of staff to maintain it unless one or more of the owners has a lot of time and interest in doing those things. It takes a lot of time and energy to keep nice homes in top condition especially if there are multiple amenities like landscaping, a pool, hot tub, and a lot of rooms to vacuum and keep clean. And to be able to pay people to do all those things without cringing or going broke takes a crazy amount of wealth to the point that you wouldn’t feel it. I don’t see myself ever getting to that point and have no need to and I’m good with that. But hey for those who are crazy rich enough to afford that, hopefully they are happy, nice people who are enjoying the fruits of their labor and wealth.

I really enjoyed this article. I’m not at this wealth level (not too far off however) but I have numerous friends who are at this level and this article nailed it. Huge denominator changes almost everything. I will say that all my friends at this wealth level made their money (not inherited or otherwise lucked into it) and they remain value-oriented and do still evaluate things like carry and opportunity cost for big purchases. Anyway, great read!

With stairs, not a bad idea to be on one level. If that is not an option, look at chair lift or in house elevator like the newer ones that use air in the same way as bank branches with multiple car bays. One caveat about chair lifts. A straight stairs is easy to do and can be relatively cheap. One that curves will be custom made and more expensive. Finally some states like Virginia offer a livable home credit. I used it for our mother in law. Still expensive but helped with about a quarter of the cost to make it livable for her.

I agree completely with your sentiment, I got cold feet last September trying to buy a home in Hermosa Beach last year ~4.5 mm…my liquid net worth was around ~16 mm at the time so it does fit your home buying guide. I guess in hindsight I do regret it a little bit because areas like this seem limited in their supply and the lost memories that I could have made with my spouse and family. My net worth has risen around 3 mm (19mm liquid net worth) not buying the house (good stock market gains plus income from my practice) so I am looking once again! Thanks for the article.

Happy hunting! It’s fun, isn’t it?

Yes, the key is to have a proper guesstimate on how much one’s net worth may grow in the future so that any big purchases today will feel more affordable, or a non-issue.

Before buying my house in 2023, I had CONSTANTLY felt like I didn’t do a good job buying the nicest house I could afford. I’ve felt this way since 2003, when I bought a $580,000 condo instead of a much nicer $920,000 condo that would have provided for a better lifestyle AND would have appreciated more too.

And I say this even after stretching to buy a house in 2005 and going through the global financial crisis. So I just decided to YOLO in 2023 and stretch to the max and blow up my passive income by ~$150,000/year.

In retrospect, if you bough the Hermosa Beach property, you probably would feel fine, if not very satisfied today given the NW growth. However, if it went DOWN $3 million to $13 million, the stress would increase for sure.

So now, at $19 million, I’d look at an upper limit of $5.7 million. Any idea how much the HB home has appreciated or not since last year?

Honestly, I see real estate in the South Bay and it’s selling at records so I’m sure it’s over 5mm….

Is South Bay another term for Hermosa Beach? If not, what is the relation between South Bay for Mehere in San Francisco? Francisco is Peninsula real estate.

If it’s over $5 million but under $5.7 million, then you’re still doing good with the ratio.

South Bay is the area Hermosa is in yes. AI programs are saying I should take and SBLOC and use the extra proceeds from my income ~ 1.5 mm per year and continue to invest it and pay if all off in 10 years. I have a 75/25 all index portfolio, I guess my worry is that the home will be 6-8 million in 10 years…

South Bay is the area Hermosa Beach is located. The math favors taking an SBLOC and use the extra proceeds from my income ~ 1.5 mm per year and continue to invest it and pay if all off in 10 years. I have a 75/25 all index portfolio, I guess my worry is that the homes will be 6-8 million in 10 years or more for that matter.

Yes Hermosa Beach is in the South Bay region. Would taking an SBLOC loan against the portfolio and using my income (~1.5 million/year) and continuing to invest be more prudent on an all index portfolio (75/25) than paying cash? In 10 years my worry is these homes will be much more.

What’s the interest rate on the SBLOC?

SOFR + 1.9%

So, I looked for that size it would be ~5.6%

Not too bad. But I dunno, as what happens if your equities correct by 20-40%? Do you need to pony up more capital?

Sam, I’d be interested in your take on a real-world capital allocation decision. My wife and I are retired with a paid-for primary residence in Washington state, where two of our adult sons and a friend live and pay rent. We also own another cash-flow-positive rental with no mortgage, and a low-carry vacant lot.

We recently moved to Wyoming and bought a modest home there.

Our total real estate is about two million with only a small amount of debt (around two hundred fifteen thousand) on a modest home we bought in Wyoming.

We may have two significant liquidity events over the next couple of years from private equity and a private company position that stems from the sale of my tech company a few years ago.

We’re considering using part of those proceeds to buy another property in Wyoming worth around one million; not as an investment or vacation home, but as a long-term primary residence that better fits how we want to live over the next few decades.

It would increase our real estate allocation, but not our leverage. At what point does owning “too much” real estate become a portfolio issue versus simply reallocating one illiquid asset into another that may provide a higher quality of life? Curious how you’d think about that trade-off.

One nuance is that the property isn’t appealing because it’s bigger or more luxurious. It’s appealing because of the land, mature infrastructure, workshops, privacy, and long-term livability. In other words, we’re buying utility more than status.

Not sure, without knowing more details, like how much liquidity is coming and total net worth. But since, you’re already retired with two adult children, the time is now to enjoy life more.

If you’re interested in doing a deep-dive consulting session with me, you can fill out the short form at the end of this page. I’m back in the mainland starting August 1.

I’ve felt the sense of urgency to live better and spend more since 45. And with the markets rebounding aggressively since 2022, that feeling to enjoy life more has only increased.